In International Shipping News 01/09/2017

The premium of up to 10 Worldscale points that LR1 tankers briefly enjoyed on the Persian Gulf-Japan route over the Red Sea-Japan route has all but disappeared, as fresh demand has emerged in the backdrop of the devastation caused by Tropical Storm Harvey in Texas, market participants said on Thursday.

“The premium no longer exists. It was there last week but is not valid anymore,” a Singapore-based chartering executive with a clean oil tankers’ owner said with reference to these routes that are popular for moving naphtha from the Middle East to North Asia.

There is more demand to load distillate cargoes for delivery into ports in the West, and this has completely reversed the situation.

On the contrary, owners will now seek premiums of 5-10 points to provide their LR1s for loading in the Red Sea, the executive said.

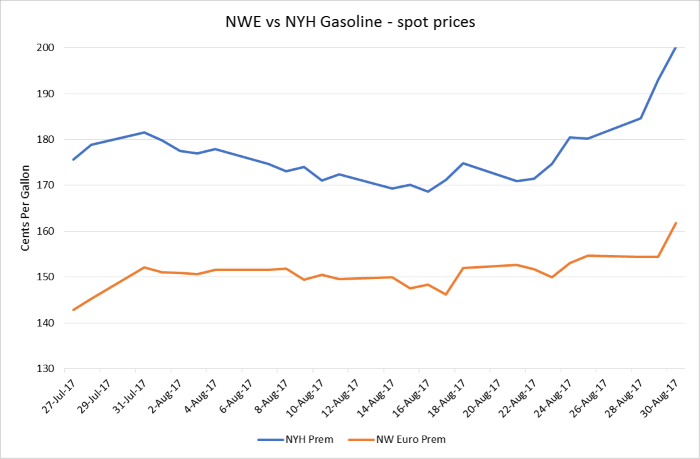

Market participants pointed out that there are now more opportunities for moving gasoil cargoes from India and the Middle East to Europe and gasoline and jet fuel cargoes to the US.

Typically, European gasoline gets shipped to the US, which in turn exports gasoil to Europe. This trade has now been disrupted by the storm in Texas. LR1s will seek employment to fill the gaps in this trade, which may not necessarily involve loading cargoes in the Red Sea.

There aren’t many ships opening in the Red Sea, which is why ballasting has to be done from elsewhere in order to load cargo in the region, an owner source said.

This ballast is unlikely to take place from Europe or East Africa and most likely to happen from Asia, which explains the possible restoration of the premium, he added.

The Red Sea-Japan LR1 on Wednesday was assessed up 10 Worldscale points at w122.5, which is on a par with the benchmark Persian Gulf-Japan rate, according to S&P Global Platts data.

Market participants said that the rates for lifting cargoes in the Red Sea are likely to be even higher now compared to the Persian Gulf rates, in the wake of the rising rates for loadings in Europe.

The LR1 rates for UK Continent-US Atlantic Coast were assessed five Worldscale points higher at w115 on Wednesday, the Platts data showed. The MR rates on the same route rose a whopping 55 Worldscale points day on day to w215 on Wednesday, the data showed.

The spike was much more significant for the MRs on the same route, as large volumes of transatlantic cargoes are transported in smaller parcels. Europe’s production of refined products is also expected to squeeze, as more than a dozen refineries will go into maintenance over the next month, thereby turning to focus into more loadings from Asia.

Also, the lifting of refined products continues unabated from the Red Sea ports of Yanbu and Rabigh, but the supply of ships is relatively tight.

The output of refined products in the Red Sea region has increased in recent years due to increasing refining capacity, such as the 400,000 b/d Yasref joint venture between Saudi Aramco and China’s Sinopec Refining Co.

The number of ships naturally opening in the Red Sea ports has not kept pace with this rising output, resulting in the premium to load in the region.

However, this trend flipped last week — only the second such instance this year after five days in late-March. But the discount did not exceed 2.5 Worldscale points at the time vis-a-vis a significant 10 points last week.

Source: Platts