In International Shipping News 31/10/2016

Eight years ago, the onset of the financial crisis following the demise of Lehman Brothers heralded a generally highly challenging time for many of the shipping markets, which today remain under severe pressure. But even within the relatively short period of history since then, different sectors have fared better or worse at various points along the way. This week’s Analysis examines the cumulative impact…

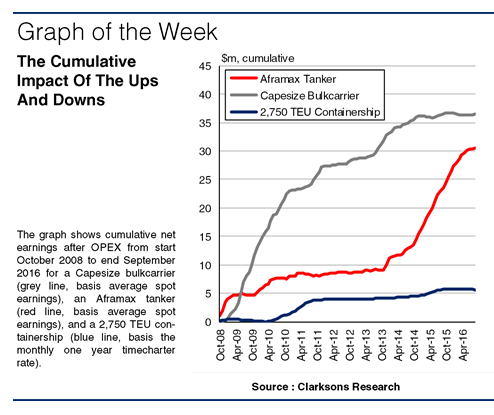

What Was The Best Bet?

So how would a vessel delivered into the eye of the financial storm in late 2008 have fared? The Graph of the Week compares the performance of three standard vessel types. It shows the monthly development of cumulative earnings after OPEX from October 2008 onwards for a Capesize bulkcarrier, an Aframax tanker and a 2,750 TEU containership.

A Capesize trading at average spot earnings would have generated around $37m in total, benefitting from market spikes in 2009-10 and 2013. But with Capesize spot earnings hovering near OPEX in recent times, the cumulative earnings have not increased much since mid-2014. For a hypothetical vessel delivered in October 2008 (and ordered at the average 2006 newbuild price of $63m) those earnings would equate to close to 60% of the contract price (note that if the vessel was sold today, this would result in a net loss of c. $8m, taking into account the earnings after OPEX, newbuild cost and sales income but not finance costs).

Totting Up Tanker Takings

By contrast, Aframax tanker earnings hovered close to OPEX for several years after the downturn, with far fewer spikes than in the bulker sector. However, the 2014-15 rally in the tanker market allowed the Aframax to start playing catch-up, and cumulative Aframax earnings between October 2008 and September 2016 reached around $31m. This represents around 50% of the value of a newbuild delivered in 2008 (with a newbuild price at the 2006 average of $63m), not too far from the ratio for the Capesize.

Bad News For Box Backers

Containerships haven’t really seen similar spikes, with the charter market largely rooted at depressed bottom of the cycle levels since 2008, battling with a huge surplus created by falling consumer demand and box trade in the immediate aftermath of the crash. With earnings close to operating costs for much of the period, a 2,750 TEU unit generated cumulative earnings after OPEX of just $6m from October 2008, around 10% of the average newbuild price in 2006 ($50m). The timecharter nature of the boxship business would also have potentially reduced owners’ upside when improved rates were on offer, and there was an ongoing chunk of capacity idle too.

The Stakes Are Still High

So, despite persisting challenging conditions overall, some of the shipping markets have seen significant ups and downs since 2008. Though boxships have seen limited income, interestingly similarly priced tanker and bulker newbuilds delivered heading into the downturn might have offered roughly comparable accumulated returns on the outlay. With conditions currently weak across most sectors, owners today would surely love to see any form of accumulation again.

Source: Clarksons