Shipping confidence reached its equal highest rating in the past three years in the three months to end-May 2017.

The average confidence level expressed by respondents to the survey was up to 6.1 out of 10.00 from the 5.6 recorded in the previous survey in February 2017. Increased confidence was recorded by all main categories of respondent to the survey, which launched in May 2008 with an overall confidence rating of 6.8.

In the case of brokers, the confidence rating rose from 4.6 to 6.4, while for owners the increase was from 5.6 to 6.1. Confidence on the part of charterers and managers, meanwhile, was up from 5.9 to 6.4, and from 6.0 to 6.2 respectively. Confidence levels were unchanged in Asia at 5.6, but up in Europe, from 5.5 to 6.2, and in North America, from 6.1 to 6.4.

A number of respondents expressed cautious optimism about the industry’s fortunes over the next 12 months, based largely on perceived increased levels of ship demolition and a rationalisation of over-ambitious newbuilding plans. This helped increase expectations of major investments being made over the next 12 months. Concern persisted, however, over political uncertainty, overtonnaging in certain trades, depressed oil prices and a potential dearth of quality seafarers.

One respondent said, “Shipping people are eternally optimistic, with one week of good news seeming to help them forget eight terrible years of hardship and financial loss.”

The likelihood of respondents making a major investment or significant development over the next 12 months was up from 4.9 out of 10.0 in the previous survey to 5.4, the highest level since August 2014. There was increased confidence on the part of all major respondents, in the case of charterers up to a level of 6.3 from 5.8 in February 2017. Owners and managers, meanwhile, each registered a confidence level of 5.9, up from 5.1 and 5.6 respectively last time. Confidence on the part of brokers was up from 3.4 to 4.4.

50% of respondents expected finance costs to increase over the coming year, compared to 54% in the previous survey. Owners’ expectations fell from 57% to 48%, while managers were also down, from 61% to 57%. More brokers and charterers, however, anticipated costlier finance – 63% of brokers (against 41% last time) and 57% of charterers (compared to 47% in February 2017). “The financial support needed to boost the markets is not yet at expected levels,” noted one respondent, “but we believe that the situation will improve in the coming months as demand increases.”

Demand trends, cited by 26% of respondents, continued to be the factor expected to influence performance most significantly over the next 12 months, followed by competition (22%) and finance costs (14%). According to one respondent, “Larger companies are targeting their smaller competitors in order to minimise competition and secure a stronger position in the market.”

The number of respondents expecting higher rates over the next 12 months was up on the previous survey in all three main tonnage categories. In the tanker market, 32% of respondents anticipated improved rates, as opposed to 25% last time, while the number anticipating lower tanker rates fell from 28% to 16%. Meanwhile, there was a 14 percentage-point rise, to 58%, in the numbers anticipating higher rates in the dry bulk sector, the highest figure for three years.

In the container ship sector, the numbers expecting higher rates rose from 31% to 46%, while there was a six percentage-point fall, to 12%, in those anticipating lower container ship rates. Net sentiment was up in the tanker market from -3 in February 2017 to +16 this time, while the increases in the dry bulk and container ship trades respectively were from +33 to +50 and from +13 to +34.

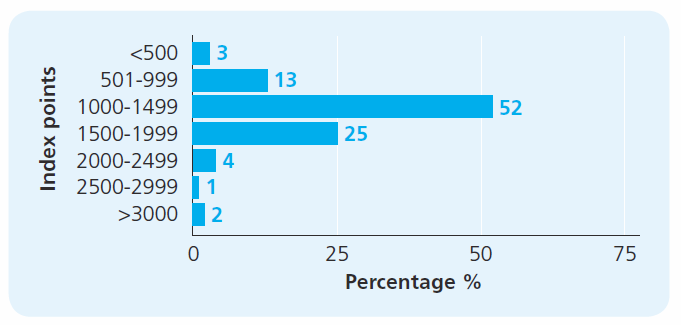

In a stand-alone question, respondents were asked to estimate the level they expected the Baltic Dry Index (BDI) to be at in 12 months’ time. More than half (52%) felt the BDI would reach a level of between 1000 and 1499, while a quarter (25%) put the likely figure at between 1500 and 1999. “Healthy volumes of cargo are being moved,” said one respondent, “but there are too many ships around.”

Richard Greiner, Partner, Shipping & Transport, says, “The survey launched in 2008, on the very cusp of one of the most protracted and severe global economic downturns, with a confidence rating of 6.8. In our latest survey, the figure stands at 6.1 which, given geopolitical, economic and industry developments, must be seen as a robust rating. Moreover, confidence today of making a major new investment is the highest it has been for almost three years. The positive sentiment on freight rates is welcome, although this must be weighed against the lows to which they have fallen and from which they must continue to recover.

“Even for an industry which is familiar with the volatile nature of international commerce, shipping’s ability to survive adversity is worthy of comment. Our latest survey found many of our respondents in watchful mode, mindful of the fact that there are still too many ships, but encouraged to believe that increased demolition and more pragmatism by industry stakeholders will help to redress this imbalance. Respondents also remain cognisant of the impact which geopolitical developments can have on shipping, and it will be instructive to see what effect all this will have on industry confidence in our next quarterly survey.”

Source: Moore Stephens